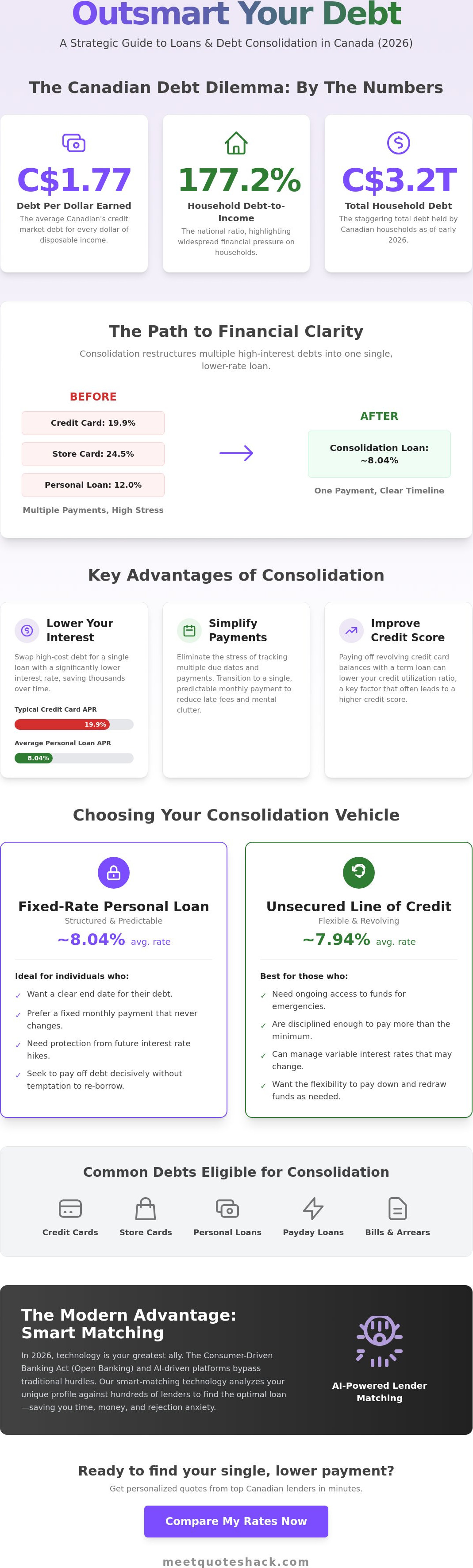

Did you know that for every dollar of disposable income, the average Canadian now carries C$1.77 in credit market debt? With total household debt hitting C$3.2 trillion in early 2026, finding an effective strategy for loans and debt consolidation has become a vital financial survival skill. You're likely tired of high interest rates consuming your paycheck and the stress of tracking multiple payment dates across different lenders. It's frustrating when the path to financial freedom feels blocked by complex terminology and shifting regulations.

We'll help you master the mechanics of consolidation and show you how to use the latest AI tools to find a lender that matches your unique risk profile. This guide explores current Bank of Canada benchmarks, explains the benefits of the new Consumer-Driven Banking Act, and provides a direct roadmap to achieving one lower monthly payment. You'll learn how to reduce your total interest paid and establish a clear, predictable timeline to becoming debt-free. It's time to stop managing your debt and start outsmarting it.

Key Takeaways

- Define debt consolidation as a strategic restructuring tool that centralizes your liabilities into a single, manageable payment.

- Compare the predictability of fixed-rate personal loans against the flexibility of unsecured lines of credit to find your ideal financial fit.

- Learn to apply the "Interest Rate Test" and calculate your Debt-to-Income ratio to ensure your new strategy delivers immediate savings.

- Streamline your approach to loans and debt consolidation by inventorying balances and utilizing smart-matching platforms to compare 2026 lender offers.

- Discover how AI-driven matching technology bypasses traditional banking hurdles to connect you with lenders tailored to your specific profile.

Understanding the Intersection of Loans and Debt Consolidation

Canadian households currently face a significant financial hurdle. As of early 2026, the household debt-to-income ratio remains high at 177.2%. This means for every dollar you earn, you likely owe C$1.77 to various creditors. When your monthly budget is stretched thin across multiple credit cards and high-interest store accounts, the strategy of loans and debt consolidation becomes a critical tool for recovery. This process isn't just about taking on a new debt; it's a deliberate financial restructuring designed to lower your overall cost of borrowing.

The mechanics are straightforward but powerful. You secure a single new loan with a lower interest rate and use those funds to pay off your existing high-cost balances. By doing this, you centralize your liability. Instead of managing five different due dates and varying interest rates, you transition to one predictable monthly payment. A foundational Understanding Debt Consolidation allows you to see this as a refinancing move rather than a simple balance transfer. It's about leveraging a lender's risk appetite to secure better terms than your original creditors provided.

Market conditions in 2026 make this a priority for many. With the Bank of Canada holding the policy interest rate at 2.25% and the prime rate sitting at 4.45%, there's a clear window to move away from credit cards that often charge 19% to 29% interest. The recent implementation of the Consumer-Driven Banking Act also empowers you to share your financial data securely with new providers. This "Open Banking" framework increases competition, making it easier to find competitive loans and debt consolidation options that match your specific profile. Don't confuse this with "debt relief" or credit counseling. While debt relief involves negotiating to pay back less than you owe (which can damage your credit score), consolidation is a proactive refinancing step that aims to keep your credit history intact while reducing interest costs.

The Core Benefits of Consolidation Loans

- Interest Rate Arbitrage: Swap 19.9% APR credit card debt for a personal loan averaging 8.04%. This move saves you thousands in interest over the life of the loan.

- Psychological Relief: Eliminate the mental "noise" of tracking multiple due dates. One payment means one deadline, reducing the risk of missed dates and late fees.

- Credit Score Growth: By paying off revolving credit card balances with a term loan, you lower your credit utilization ratio. This often leads to a measurable boost in your credit rating within a few months.

Common Debts Eligible for Consolidation

Most unsecured liabilities can be folded into a single plan. High-interest credit card balances and retail store cards are the primary targets for consolidation. You can also include existing unsecured personal loans or high-cost payday alternatives that carry rates near the legal 35% APR cap. Even outstanding utility arrears or medical bills can often be rolled into the new loan to help you regain control of your monthly cash flow.

Comparing Consolidation Vehicles: Personal Loans vs. Lines of Credit

Selecting the right vehicle for loans and debt consolidation is a strategic decision that dictates your financial trajectory for the next several years. You generally face two primary paths: the structured predictability of a personal loan or the fluid flexibility of a line of credit. In the current May 2026 market, unsecured lines of credit carry an average interest rate of 7.94%, while personal loans hover around 8.04%. While the rates are similar, the impact on your daily budget and repayment behavior differs significantly.

A personal loan provides a lump sum to wipe out high-interest creditors immediately. You then follow a rigid amortization schedule until the balance reaches zero. Conversely, a line of credit allows you to draw funds as needed. This flexibility is useful for managing ongoing expenses, but it requires high discipline to avoid re-accumulating debt. To help you weigh these options, the Government of Canada's guide to debt consolidation offers an excellent framework for understanding how these products interact with your credit report and overall financial health.

When a Fixed-Rate Personal Loan Wins

Fixed-rate loans are the gold standard for Canadians seeking a definitive exit from debt. Because the interest rate is locked, you are shielded from any potential hikes in the Bank of Canada’s 2.25% policy rate. This stability allows you to circle a date on your calendar 36 or 60 months from today and know exactly when you will be debt-free. It removes the temptation of a revolving balance. Once you pay it down, the "room" does not open back up for new spending. This structure is often the safest path for those who want to simplify their life. You can check how much you pre-qualify for to see if a fixed-rate option fits your monthly cash flow.

The Role of Home Equity in Debt Strategy

If you own property, your home equity is your most potent tool for restructuring. Secured lines of credit (HELOCs) currently average 4.07%, which is roughly half the cost of unsecured options. Refinancing your mortgage to absorb consumer debt can drastically lower your monthly overhead and provide immediate breathing room. However, this strategy carries weight. You are moving unsecured debt into a secured loan backed by your primary residence. It is a high-stakes move that requires careful navigation of the federal "stress test" requirements. Many homeowners find it beneficial to find mortgage advisors who specialize in debt-centric refinancing to ensure the long-term math actually works in their favor.

Strategic Evaluation: Is a Consolidation Loan Right for You?

Before committing to loans and debt consolidation, you must perform a cold, technical assessment of your financial health. Lenders in 2026 look closely at your Debt-to-Income (DTI) ratio. This is the percentage of your gross monthly income that goes toward paying debts. Generally, Canadian lenders prefer a DTI below 40% for unsecured products. If your ratio exceeds this, you might need to explore secured options or adjust your target loan amount. Use the Financial Consumer Agency of Canada resources to benchmark your current standing against national standards.

Run the "Interest Rate Test" next. A consolidation loan only makes sense if the new APR is lower than the weighted average of your current debts. With the average personal loan rate at 8.04%, moving debt from a 22% retail card is an obvious win. However, moving a 9% line of credit to an 8.5% loan might not be worth the effort once you factor in administrative costs. You also need to evaluate your behavior. A loan clears the balance; it doesn't fix the spending habits that created the debt. If you don't stop using the original cards, you risk "double-dipping" and doubling your total liability.

Assessing Your Credit Readiness

Lenders want more than just a high score. They prioritize a "clean" payment history for the last 12 months. Any recent late payments can trigger higher rates or outright denials, even if your total score seems adequate. Modern platforms allow you to check how much you pre-qualify for using soft credit pulls. This lets you see potential rates without a hard inquiry hitting your report. It's an efficient way to shop for loans and debt consolidation without damaging your credit standing during the search.

The Hidden Costs of Consolidation

Watch for the friction points. Some Canadian lenders charge origination fees ranging from 1% to 5% of the total loan amount. These fees are often deducted from the payout, meaning you receive less than you applied for. Always check for pre-payment penalties as well. If you receive a bonus or tax refund, you want the freedom to pay down your principal faster without being penalized. Staying vigilant about these terms ensures that your path to being debt-free remains as fast and inexpensive as possible.

Navigating the Canadian Lending Process in 2026

The process for securing loans and debt consolidation has evolved significantly with the 2026 rollout of Open Banking under Bill C-15. You no longer need to spend weeks gathering paper statements or visiting multiple bank branches. Efficiency is the new standard. To begin, build a precise inventory of your current liabilities. List every balance, the specific APR, and the monthly minimum payment. This data serves as the foundation for your strategy. It allows you to see exactly where high interest is eroding your wealth, especially with total household debt in Canada sitting at C$3.2 trillion.

Once your data is ready, utilize smart-matching platforms to compare multiple lender offers at once. These tools use AI to match your specific risk profile with lenders that have the highest appetite for your debt type. When you receive offers, look past the monthly payment amount. Focus instead on the "Total Cost of Borrowing" disclosure. This mandatory Canadian document reveals the total interest and fees you'll pay over the entire term. After selecting a path, you can finalize the application through digital document verification. This secure framework has replaced outdated methods like "screen scraping," ensuring your financial data moves safely between institutions. Finally, ensure the loan proceeds reach your creditors directly to stop the interest clock immediately.

The Advantage of Online Marketplaces

Speed and precision define the modern lending landscape. Online marketplaces can often move you from application to funding in 24 to 48 hours. This is a massive shift from traditional banking timelines. These platforms also provide essential access to "B-lenders" and non-bank institutions. These lenders often have more flexible criteria than the Big Five banks, making them vital for diverse financial profiles. QuoteShack’s AI smart forms streamline this even further by reducing manual entry and improving data accuracy. You can check how much you pre-qualify for in minutes to see how these technological advances work for you.

Regional Considerations: Debt Solutions in BC vs. Ontario

Geography influences your consolidation options. Provincial regulations in Ontario and British Columbia can impact loan availability and maximum allowable fees. If you're using home equity as part of your strategy, local expertise is non-negotiable. Mortgage advisors with regional knowledge understand the specific property market trends that lenders use to calculate your loan-to-value ratio. For those in the West, exploring Debt Consolidation BC: Solutions for Western Canadians can provide the localized insight needed to navigate the Pacific market's unique conditions. Matching your strategy to your province ensures you don't miss out on regional incentives or protections.

The QuoteShack Advantage: Smart Matching for Debt Relief

Traditional banking often relies on a rigid, one-size-fits-all model that fails to account for the diverse financial realities of modern Canadians. When you walk into a branch, you're limited to their specific products and risk appetite. If your profile doesn't fit their narrow box, you're left with a rejection and a hard inquiry on your credit report. QuoteShack changes this dynamic by leveraging a marketplace approach. Instead of you chasing a single bank, our network of lenders competes for your business. This competitive environment ensures you find the most efficient loans and debt consolidation options tailored to your specific financial situation.

Empowerment comes through transparency. Our platform uses AI smart forms to analyze your data and match you with lenders that actually want to fund your profile. This precision reduces the friction often found in the Canadian lending space. By using pre-qualification tools, you gain the clarity needed to make a decision without committing to a hard credit pull. You see your standing upfront. This technological sophistication removes the guesswork, allowing you to move forward with a partner that has already performed the heavy lifting of vetting potential matches.

Seamless Integration with Auto and Home Loans

Your financial life isn't lived in a vacuum. Often, the need for debt restructuring overlaps with other life goals, such as upgrading a vehicle or managing a mortgage. Our network allows you to explore auto loans and personal debt management simultaneously. If you're a homeowner, the platform can help you find mortgage advisors who specialize in debt-centric refinancing. The QuoteShack dashboard provides a clear, real-time view of your progress, creating a transparent bridge between you and your chosen lender. This centralized hub ensures every part of your financing strategy moves in sync.

Taking the First Step Toward Financial Freedom

Waiting is the most expensive decision you can make when dealing with high-interest liabilities. Every day of hesitation adds to the C$3.2 trillion in total household debt Canadians are already carrying. You've learned the mechanics of loans and debt consolidation and understood how to evaluate your DTI ratio. Now it's time to execute. Transitioning from high-interest stress to a single, smart payment is a matter of clicks, not weeks. Take control of your momentum and Check how much you pre-qualify for today to begin your journey toward a debt-free future.

Secure Your Financial Momentum Today

You now have the roadmap to move from fragmented high-interest debt to a streamlined, strategic plan. By prioritizing loans and debt consolidation, you effectively lower your borrowing costs and reclaim control over your monthly cash flow. The 2026 financial landscape rewards those who use technology to their advantage. Don't let high interest rates stall your progress when modern tools can bridge the gap between where you are and where you want to be.

QuoteShack simplifies this transition. Our AI-powered smart matching identifies better rates tailored specifically to your financial profile. You can also connect with a network of professional Canadian mortgage advisors for complex home-based strategies. The process is fast and transparent. You can check your standing and explore options without a hard credit pull impacting your score. It's about removing friction and replacing it with certainty.

See your personalized loan matches and pre-qualify in minutes. Your path to a debt-free life is closer than it was this morning. Take the first step toward lasting financial clarity and start building your future on solid ground.

Frequently Asked Questions

Will a debt consolidation loan hurt my credit score?

You might see a small, temporary dip in your score due to the hard credit inquiry during the final application phase. This is normal and happens with almost any new credit application. Most Canadians find their score improves quickly as they pay off revolving credit card balances and lower their overall credit utilization ratio. Using a term loan to clear high-interest cards often shows lenders you're managing your liabilities more effectively.

What is the difference between a debt consolidation loan and a personal loan?

A debt consolidation loan is essentially a personal loan used for a specific purpose. While the financial product is often the same, the consolidation version is designed to pay off multiple creditors at once. Some lenders even offer to pay your creditors directly to ensure the funds are used as intended. It's a targeted strategy rather than a general-purpose loan.

Can I get a consolidation loan with a low credit score in Canada?

Yes, you can still find options. While the Big Five banks have strict requirements, many alternative lenders in Canada specialize in helping borrowers with diverse credit profiles. You might face a higher interest rate than someone with a prime score, but these loans still provide an opportunity to simplify your budget and begin rebuilding your credit history through consistent, on-time payments.

How much can I save by consolidating my credit card debt?

Your savings depend on the difference between your current interest rates and your new loan's APR. Moving a C$10,000 balance from a 22% retail card to an 8.04% loan can save you thousands of dollars in interest over the life of the term. This reduction in interest costs allows more of your monthly payment to go toward the principal balance, helping you become debt-free much faster.

Are online lenders safe for debt consolidation?

Reputable online lenders are highly secure and must follow strict provincial and federal regulations. The 2026 Open Banking framework in Canada has further enhanced security by moving away from risky data-sharing methods. Modern platforms use bank-grade encryption and digital verification to protect your personal information while providing a faster, more efficient experience than traditional branches.

What happens if I am declined for a consolidation loan?

Don't panic if your first application is unsuccessful. Review the lender's "adverse action" notice to understand why you were declined, as it's often related to a high debt-to-income ratio or recent credit issues. You can then use a matching platform to find a lender with a different risk appetite or consider a secured loan if you have assets like a vehicle or home equity to leverage.

Is it better to refinance my mortgage or get a personal loan for debt?

Mortgage refinancing typically offers the lowest interest rates, often around the 4% to 5% range in 2026. However, this moves unsecured debt to a secured asset, which means your home is at risk if you default. A personal loan is better for smaller amounts of debt or for those who don't want to reset their mortgage term or pay potential prepayment penalties.

How long does it take to get approved for a consolidation loan through QuoteShack?

The process is designed for maximum speed. You can see pre-qualification offers for loans and debt consolidation in just a few minutes through our AI-driven platform. Once you select a lender and complete the digital document verification, final approval and funding often occur within 24 to 48 hours. It's a streamlined path that respects your time and your need for immediate relief.