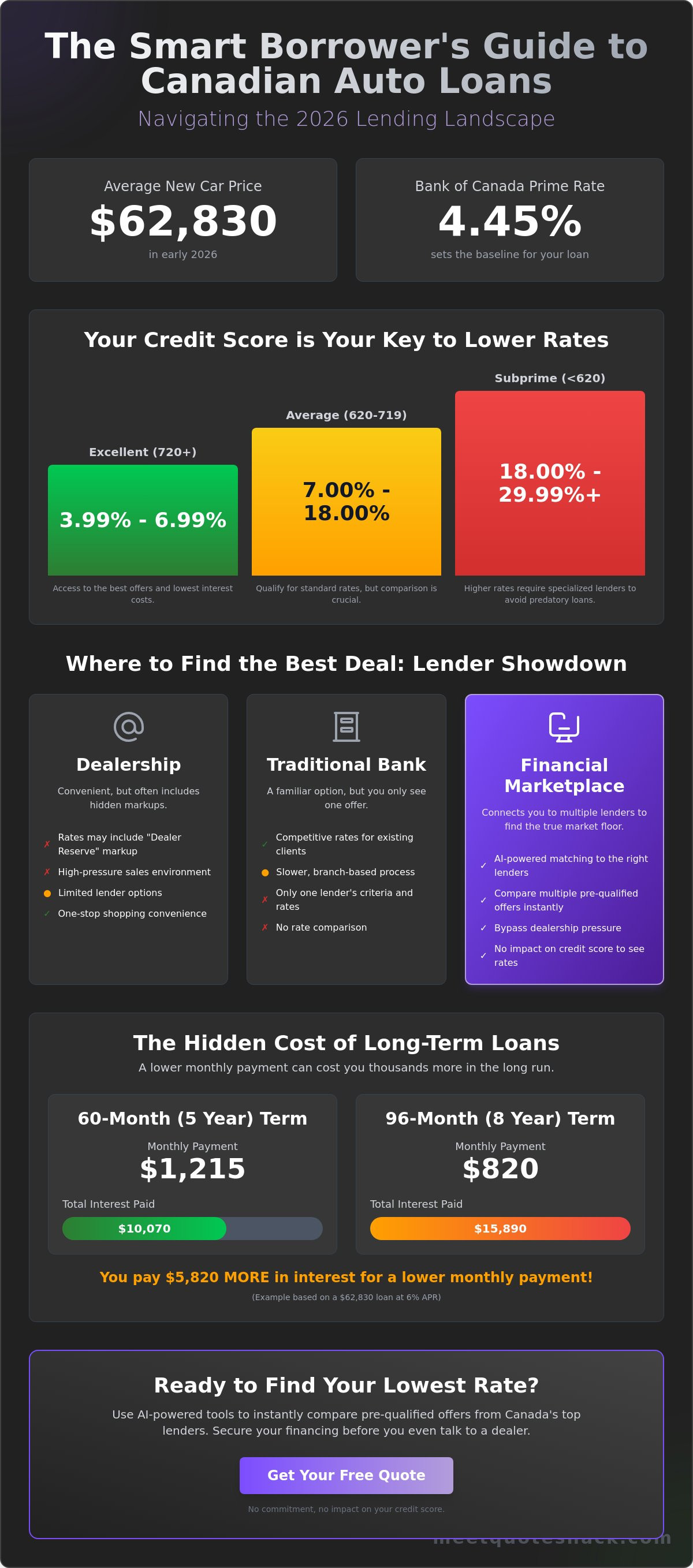

If you walk into a dealership relying solely on their "best offer," you're likely overpaying by thousands. In 2026, blind loyalty to your primary bank is effectively a tax on your vehicle purchase. Finding the true market floor for auto loans requires a shift from passive acceptance to smart, data-driven intelligence. You've likely felt the pressure of the current economy. With the average new car price reaching $62,830 and the Bank of Canada prime rate holding at 4.45%, securing an affordable payment feels like a high-stakes gamble. It's exhausting to face aggressive finance offices or worry that shopping around will damage your credit score just when you need it most.

We've designed this guide to remove that friction and put the power back in your hands. You'll learn how to secure the lowest possible interest rate and identify the critical difference between a low monthly payment and the actual total cost of ownership. We'll break down the 2026 lending landscape, compare lender types, and show you the smartest way to pre-qualify before you ever hit the lot.

Key Takeaways

- Master the 2026 regulatory environment and understand how the Bank of Canada prime rate directly affects your borrowing costs.

- Avoid long-term debt traps by balancing monthly payments against the total interest cost over the life of the loan.

- Uncover hidden dealership markups like "Dealer Reserves" to ensure you pay the true market floor for your financing.

- Implement a five-step strategy to secure auto loans at the lowest possible rates, leveraging precise credit bureau insights.

- Utilize AI-powered matching tools to connect with the right lenders instantly and bypass the high-pressure dealership finance office.

Table of Contents

Navigating the Canadian Auto Loan Landscape in 2026

In Canada, Car finance is governed by provincial regulations that protect your rights as a borrower. Most auto loans are secured agreements. This means the vehicle itself acts as collateral for the debt. This structure provides a safety net for lenders, which typically results in lower interest rates compared to unsecured personal loans. However, it also means the lender has a legal claim to the car if you default on payments. In 2026, the industry has pivoted toward digital-first models. These platforms prioritize borrower transparency over traditional dealership profit margins.

Choosing a secured loan is often the smartest way to minimize your total interest expense. While personal loans offer flexibility, they lack the asset backing that keeps car-specific financing affordable. Modern Canadian borrowers now look for pre-qualification tools that provide clarity before they ever step onto a lot. This proactive approach prevents the high-pressure tactics often found in traditional finance offices.

Why the Prime Rate Matters for Your Car Payment

The Bank of Canada (BoC) sets the foundation for your monthly bill. In early 2026, the BoC policy rate has stabilized at 2.25% after a period of volatility. This translates to a Prime Rate of 4.45% at most major financial institutions. Prime Rate is the baseline for all consumer lending. When this rate shifts, variable-rate auto loans fluctuate immediately, changing your interest portion overnight. Fixed-rate loans offer protection against these shifts but usually carry a slightly higher starting percentage. Understanding this link helps you time your application. A stable overnight rate suggests it's a safe time to lock in a term without fear of immediate spikes.

The Rise of the Financial Marketplace

Canadians are moving away from traditional branch-based applications. Walking into a single bank limits your options to one set of lending criteria. Modern fintech marketplaces like QuoteShack change the dynamic entirely. We use AI-powered smart forms to connect you to a broad network of lenders simultaneously. This digital-first approach focuses on pre-qualification. You see your potential rates without a hard credit pull. It removes the guesswork from the process. Borrowers now demand this level of intelligence. They want to compare multiple offers in minutes. This shift toward marketplace lending ensures you find the true market floor for your rate, bypassing the "dealer reserve" markups common in the past.

Decoding Interest Rates, Terms, and Total Cost of Ownership

Understanding the mechanics of auto loans prevents expensive surprises at the end of your term. Every agreement rests on three pillars: the principal, the APR, and the term. The principal is the total amount you borrow. The APR includes both the interest rate and any lender fees, representing the true cost of borrowing. The term is the duration of your repayment. While many buyers fixate on the monthly payment, the total cost of ownership tells the real story. This figure encompasses interest, insurance, and maintenance over the life of the vehicle. For a new car averaging $62,830 in early 2026, even a minor APR fluctuation can cost you thousands. Your credit score is the primary lever for these rates. Borrowers with excellent scores (720+) typically secure rates between 3.99% and 6.99%. Conversely, subprime borrowers with scores below 620 may face rates exceeding 29.99%. Reviewing the Government of Canada car financing guide provides a solid baseline for your consumer rights before you sign.

Fixed vs. Variable Rates: Which is Safer in 2026?

Fixed rates provide absolute certainty. You lock in a specific percentage, and your payment remains identical for the entire term. This is the preferred choice for Canadians who need strict budget predictability. Variable rates are tied to the prime rate, which currently sits at 4.45% at major banks. These rates might start lower than fixed options but carry the risk of increasing if the Bank of Canada adjusts its policy. If you have a high risk tolerance and a flexible budget, riding the market might save you money if rates drop. However, most 2026 buyers opt for fixed rates to avoid the stress of market volatility. You can check how much you pre-qualify for to see which rate structure aligns with your financial profile.

The Hidden Cost of Long-Term Financing

Extending your loan to 84 or 96 months is a common tactic to make expensive vehicles feel affordable. It is also a significant debt trap. A 96-month loan on a C$60,000 vehicle results in significantly higher total interest compared to a 60-month term. Long terms also lead to negative equity. This occurs when your loan balance stays higher than the car's rapidly depreciating market value. If you need to sell the car early, you'll have to pay the lender the difference out of pocket. A 60-month term is the ideal "sweet spot" for most Canadian vehicles. It ensures you build equity faster and pay less to the bank over time.

Dealership vs. Bank vs. Marketplace: Where is the Best Deal?

Selecting a lender requires more than just a signature. Most Canadian buyers choose between three main paths: the dealership finance office, a traditional bank branch, or a digital marketplace. Each has distinct advantages, but the costs vary wildly. Dealerships prioritize convenience but often include a "Dealer Reserve." This is a hidden markup added to the interest rate provided by the bank. If a bank offers the dealer a 5% rate, the dealer might present it to you as 6.5%. That 1.5% difference is pure profit for the dealership. Information from the Financial Consumer Agency of Canada highlights how these agreements impact your long-term financial obligations.

Marketplaces represent the modern alternative. QuoteShack acts as a neutral facilitator rather than a lender. We use technology to scan multiple institutions simultaneously, ensuring you see the true market floor. This transparency removes the conflict of interest found in dealership offices. By using a marketplace, you secure a baseline rate that serves as a powerful negotiation tool if you eventually decide to finance through a dealer. It puts the leverage back in your hands before you ever set foot on the lot.

The Truth About Dealership Financing

Dealerships often work with "captive lenders." These are the financial arms of manufacturers, such as Toyota Financial Services. They frequently offer aggressive 0% or 1.99% incentives to move new inventory. These rates are excellent if you qualify. However, for most used auto loans, dealers act as brokers for big banks. Beware of "spot delivery" tactics. This occurs when a dealer lets you drive the car home before the bank has officially signed off on the loan. If the bank later rejects the application, the dealer may force you into a much higher interest rate. Always walk into the F&I office with a pre-approval in hand. It forces the dealer to beat an existing offer rather than setting an arbitrary price.

Why Your Primary Bank Might Not Be the Best Option

Loyalty rarely pays in the lending world. Banks manage "risk concentration." If you already hold a mortgage and several credit cards with one institution, they may view an additional car loan as too much exposure. This can lead to higher rates or even a rejection, regardless of your credit score. Alternative lenders and smaller credit unions often have different risk appetites. They may offer more competitive terms for your specific profile. QuoteShack’s AI-driven system scans these diverse options instantly. We find the lenders who are currently hungry for your business, regardless of where you do your daily chequing. This ensures you aren't penalized for having all your financial eggs in one basket while searching for auto loans.

The 5-Step Strategy to Secure Your Lowest Auto Loan Rate

Stop letting dealerships dictate your financial future. Flipping the traditional car-buying process saves you money and significant stress. By securing your financing first, you enter the lot as a "cash buyer" with total leverage. This five-step strategy ensures you find the most competitive auto loans without falling for common industry traps.

-

Verify your credit data. Check your score through Equifax or TransUnion. In Canada, a score above 720 unlocks the lowest interest rates, while anything below 620 requires a more specialized lending approach.

-

Calculate your real budget. New vehicle prices in 2026 average C$62,830. Use digital tools to determine what you can actually afford before looking at inventory.

-

Set your rate ceiling. Get pre-qualified to see your potential APR. This number is your benchmark that no dealer should exceed.

-

Shop with confidence. Focus on the vehicle's "out-the-door" price. You already have the money; now you're just finding the right asset.

-

Verify the contract. Before signing, ensure the APR and total interest costs match your pre-qualification exactly.

Pre-Qualification vs. Pre-Approval: Knowing the Difference

Protecting your credit score is vital. A pre-qualification uses a "soft hit" on your credit report. It provides an estimated rate without lowering your score. QuoteShack uses AI smart forms to scan lenders while keeping your credit profile intact. A "hard hit" or hard inquiry only occurs when you officially apply to a specific lender to finalize the deal. This distinction allows you to shop for auto loans with complete peace of mind. You can check how much you pre-qualify for today to establish your baseline without any credit damage.

Negotiating Like a Pro with a Quote in Hand

Dealership finance managers often ask, "What monthly payment are you looking for?" This is a trap designed to hide high interest rates or long loan terms. Your response should be firm. Tell them, "I'm focused on the total out-the-door price and a specific APR." Having a pre-qualification quote in hand changes the conversation. It forces the dealer to compete with an existing offer. If they can't beat your marketplace rate, you simply use your own financing. This professional approach removes the emotional pressure and keeps you in control of the final numbers.

How QuoteShack Simplifies Your Path to the Driver's Seat

QuoteShack is the modern response to an outdated, manual system. We serve as a high-tech facilitator. Our platform removes the friction from traditional auto loans by replacing tedious paperwork with streamlined intelligence. Because we are a marketplace and not a direct lender, we offer a completely transparent view of the lending landscape. This ensures you aren't limited by the narrow risk appetite of a single bank. We provide a simplified path forward by doing the complex background work for you. Our goal is to empower every Canadian borrower with the same data tools used by industry professionals.

Our lender lead management dashboard provides a centralized hub for your entire financing journey. You no longer need to track dozens of emails or manage multiple phone calls from different institutions. The dashboard organizes every offer with professional precision. It allows you to compare APRs, monthly payments, and total interest costs side-by-side. This level of organization provides the relief of knowing you've seen every option. It empowers you to make a decision based on cold, hard data rather than dealership pressure. You remain in total control of the process from the initial search to the final signature.

Smart Forms and Instant Eligibility

Our AI-powered smart forms are designed for speed and security. You provide your information once. Our system then processes that data to determine your eligibility across our entire network instantly. This eliminates the need for redundant bank visits and repetitive data entry. It also protects your data accuracy. Our technology ensures that your profile is presented to lenders who are most likely to approve your application based on current 2026 market conditions. This targeted approach saves you hours of manual research. It prevents unnecessary credit inquiries and ensures your path to a new vehicle is as fluid as possible.

Connecting You with Canada’s Top Lenders

Competition is the only way to drive down borrowing costs in a high-rate economy. QuoteShack’s network includes major Canadian banks, regional credit unions, and specialized niche lenders. Each institution competes for your business. This competitive environment is what allows us to find the lowest rates available. Whether you are looking for auto loans for a new C$62,830 truck or a reliable used sedan, our network covers the full spectrum of the market. This breadth ensures that borrowers across all credit tiers find a path forward. We provide the intelligence you need to bypass markups and secure the best possible terms. Check how much you pre-qualify for today.

Take Command of Your Automotive Future

Mastering the Canadian finance market in 2026 requires a shift from passive browsing to active intelligence. You now understand that bank loyalty is often a tax and that dealership markups are avoidable with the right preparation. Prioritizing the total cost of ownership over tempting monthly payments ensures your vehicle remains a manageable asset rather than a debt trap. By following a consumer-first strategy, you secure auto loans that align with your long-term financial goals rather than a salesperson's monthly quota.

QuoteShack is here to remove the friction from this traditionally complex process. Our platform uses AI-powered smart matching to connect you with a nationwide network of Canadian lenders instantly. You get the clarity of a no-impact credit pre-qualification, allowing you to shop with a firm rate ceiling already in place. It's time to replace uncertainty with data-driven confidence. Check how much you pre-qualify for with QuoteShack and step onto the lot with the leverage you deserve. Your next car is waiting, and you finally have the tools to claim it on your own terms.

Frequently Asked Questions

What is a good interest rate for an auto loan in Canada in 2026?

A good interest rate for borrowers with excellent credit (720+) currently ranges from 3.99% to 6.99%. The market average for new auto loans in early 2026 is approximately 6.5%. These rates are influenced by the Bank of Canada prime rate, which currently sits at 4.45% at most major institutions. Securing a rate below the 6.5% average typically requires a strong credit history and a shorter repayment term.

Does applying for an auto loan quote through QuoteShack hurt my credit score?

No, checking your rate through QuoteShack uses a soft credit inquiry that has zero impact on your credit score. Our AI smart forms allow you to see potential offers without the "hard hit" that traditional bank applications require. You only face a hard credit inquiry once you choose a specific lender and move forward to finalize the actual loan contract.

Can I get an auto loan in Canada with a 600 credit score?

Yes, you can secure a loan with a 600 credit score, though you will likely be classified as a subprime borrower. In the 2026 market, borrowers with scores below 620 typically see interest rates ranging from 10.99% to 29.99%. Using a marketplace is especially helpful for this credit tier. It allows you to find specialized lenders who look at your total financial picture rather than just a single number.

What is the maximum term for a car loan in Canada?

Most Canadian lenders offer maximum loan terms of 84 to 96 months. While these extended terms lower your monthly payment, they significantly increase the total interest you pay over time. Many borrowers with 96-month terms find themselves in "negative equity," where the car's value drops faster than the loan balance. Aiming for a 60-month term is the safest way to build equity quickly.

Is it better to get a car loan from a bank or a dealership?

It depends on the incentives available, but a marketplace usually provides the most transparency. Dealerships offer convenience and manufacturer incentives, but they often add a "Dealer Reserve" markup to bank rates. Banks provide stability but may limit your borrowing if you already have other products with them. Getting pre-qualified through a marketplace first gives you the leverage to negotiate with both parties effectively.

Can I pay off my auto loan early without penalties in Canada?

Most modern auto loans in Canada are "open" contracts, which means you can pay them off at any time without a penalty. This allows you to make extra payments toward the principal to save on total interest. Always verify the "Prepayment" clause in your specific agreement before signing to ensure there are no hidden administrative fees for early closure.

What documents do I need to apply for an auto loan online?

You will need a valid Canadian driver's license, proof of residency (like a utility bill), and proof of income. Most lenders require your two most recent pay stubs or a formal employment letter. If you are self-employed, you may need to provide your Notice of Assessment from the CRA. Having digital copies of these documents ready ensures the AI-powered matching system can verify your eligibility instantly.

How does the Bank of Canada prime rate affect my existing car loan?

The prime rate only affects you if you have a variable-rate loan. If your rate is variable, your interest will fluctuate whenever the Bank of Canada adjusts its policy rate, which currently keeps the prime rate at 4.45%. If you have a fixed-rate loan, your payment and interest rate are locked in for the duration of the term, regardless of how the prime rate moves.