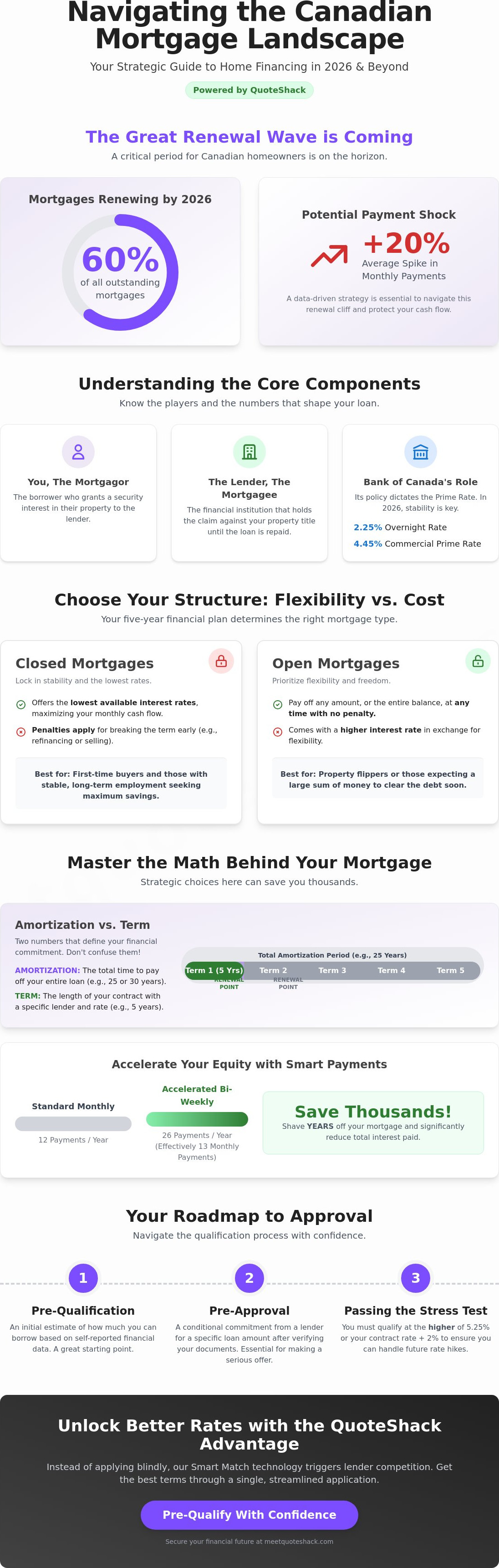

About 60% of all outstanding mortgages in Canada are scheduled to renew by the end of 2026. This means more than half of the country is approaching a renewal cliff where monthly payments could spike by an average of 20%. Securing a mortgage loan in this climate requires more than just luck; it demands a data-driven strategy that prioritizes your long-term cash flow over a flashy headline rate.

You're likely feeling the pressure of the 5.25% stress test or worrying about how fluctuating interest rates will impact your monthly budget. It's frustrating when the rules change just as you're ready to make a move. We've designed this guide to remove that friction and empower your decision-making. You'll learn how to master the complexities of Canadian financing and find the smartest path to homeownership while avoiding hidden fees.

We'll break down the latest 3.35% variable options, explain how first-time buyers can leverage the new 30-year amortization rules, and provide a clear roadmap to help you pre-qualify with total confidence. Let's transform your financing into a strategic tool for growth.

Key Takeaways

- Master the legal mechanics of a mortgage loan to understand how property collateral and lender agreements impact your ownership rights.

- Learn how to optimize amortization periods and payment frequencies to minimize total interest and accelerate your path to being debt-free.

- Compare fixed-rate certainty with variable-rate Prime Rate fluctuations to select the financing structure that best fits your household budget.

- Navigate the approval process with precision by distinguishing between pre-qualification and pre-approval before you start your home search.

- Leverage intelligent marketplace tools to trigger lender competition, securing better terms through a single, streamlined application.

What is a Mortgage Loan? Understanding the Canadian Framework

A mortgage loan is more than a simple monthly bill; it's a legal agreement where your property serves as collateral. In this framework, you are the mortgagor, the individual granting the security interest. The lender is the mortgagee, the entity holding the claim against the title. Understanding What is a Mortgage Loan? helps you realize that the lender is essentially your silent partner until the balance hits zero. This legal structure protects the lender's investment while giving you the capital needed to secure a high-value asset.

The 2026 market demands a tech-forward approach to these traditional roles. Manual paperwork and long wait times have been replaced by automated systems that prioritize speed and accuracy. We focus on a "Smart Match" concept. Instead of applying blindly, your financial data is matched with lender portfolios that specifically want your type of profile. This removes friction and increases your odds of approval. You can check how much you pre-qualify for using our digital tools, ensuring you only talk to lenders who fit your specific needs.

The Role of the Bank of Canada and Prime Rates

The Bank of Canada influences your borrowing costs through the "overnight rate." This is the interest rate at which major financial institutions borrow and lend one-day funds among themselves. In 2026, the central bank maintains this policy rate at 2.25%. This stability flows directly into the Prime Rate, which sits at 4.45% across most major Canadian institutions. If you hold a variable-rate mortgage, your interest rate is expressed as "Prime plus" or "Prime minus" a certain percentage. When the central bank stays steady, your variable payments remain predictable, allowing for better long-term budgeting.

Open vs. Closed Mortgages: Flexibility vs. Cost

Deciding between an open or closed mortgage loan depends on your five-year financial horizon. The choice dictates how much you'll pay and how easily you can exit the contract.

- Closed Mortgages: These offer the lowest available interest rates. In exchange for the discount, you agree to stay with the lender for the full term. Breaking this contract early to refinance or sell usually triggers a penalty based on three months' interest or the Interest Rate Differential.

- Open Mortgages: These provide ultimate flexibility. You can pay off the entire balance or sell the property at any time without paying a cent in penalties. However, you'll pay a higher interest rate for this freedom.

If you're a first-time buyer in a stable job, a closed mortgage usually provides the best value. If you're planning to flip a property or expect a large inheritance to clear the debt, the open route is the smarter move. Most Canadians opt for closed terms to lock in lower costs during their initial years of homeownership.

Decoding the Mechanics: Amortization, Terms, and Payments

Understand the math behind your mortgage loan before signing the contract. Most Canadians confuse the "term" with "amortization," but these two numbers dictate your financial freedom. The term is your legal commitment to a specific rate and lender, while amortization is the total time it takes to pay off the debt. Aligning these two factors correctly ensures your home remains an asset rather than a burden.

Your down payment size serves as the foundation of this structure. Putting down 20% or more allows you to avoid mortgage default insurance, whereas a smaller down payment requires an insured loan. In 2026, all applicants must pass the mortgage stress test. This regulation requires you to qualify at the higher of 5.25% or your contract rate plus 2%. It's a safety buffer designed by the government to ensure you can handle future rate hikes without defaulting on your obligations.

Accelerate your equity by adjusting your payment frequency on your mortgage loan. Switching from monthly to accelerated bi-weekly or weekly payments effectively adds one extra monthly payment per year. This simple shift can shave years off your debt and save you thousands in interest charges over the life of the contract. It's a high-impact strategy that requires zero change to your interest rate but yields significant long-term savings.

Amortization: The Long-Term Vision

Select your amortization period based on your cash flow priorities. A standard 25-year amortization is the baseline for most, but as of late 2024, first-time buyers can access 30-year amortization on insured mortgages. This longer window lowers your monthly commitment, providing breathing room in a high-cost environment. However, a shorter 25-year window builds equity faster and reduces total interest costs. We help loanees visualize these long-term impacts through intelligent data modeling so you can choose the path that fits your lifestyle.

Mortgage Terms: The Renewal Cycle

Think of your mortgage term as a series of short-term contracts within the Canadian mortgage framework. The 5-year fixed term remains the most popular choice for its stability, but 2026 sees a rise in 1-3 year short-term renewals. These shorter terms are tactical moves for those waiting for rates to drop further. With 60% of all outstanding mortgages renewing in 2025 and 2026, many homeowners face "renewal shock." Prepare for this by reviewing your options six months before your term ends. You can compare current market offers to ensure your next term is as efficient as the first.

Fixed vs. Variable Rates: Navigating Your Options

Choosing between a fixed or variable mortgage loan determines your financial rhythm for the next five years. It's a decision that balances the psychological need for certainty against the potential for interest savings. While one offers a locked-in shield against market volatility, the other provides a dynamic path that can lower your costs if economic conditions soften.

Families in growing hubs like Brampton or Surrey often prioritize the fixed-rate model. With the best 5-year fixed rates sitting at approximately 4.04% as of May 2026, this option removes the guesswork from monthly budgeting. You aren't just buying a home; you're buying a predictable expense. This certainty is crucial for those managing tight household margins where even a small increase in debt service could disrupt other financial goals.

Variable rates offer a different advantage. These products fluctuate alongside the Prime Rate, which currently stands at 4.45%. If you select a variable rate of 3.35%, you're starting with a significant discount compared to fixed options. For those who believe the Bank of Canada has finished its hiking cycle, this is the most efficient way to pay down principal faster. If you're undecided, a hybrid mortgage loan splits your balance into two segments: one fixed and one variable. This creates a diversified portfolio within a single agreement, mitigating risk while keeping the door open for potential savings.

When to Choose a Fixed-Rate Mortgage

Fixed-rate terms are the primary choice for risk-averse borrowers. In 2026, the Canadian market shows a trend toward stability, but high-cost centers like Toronto and Vancouver still carry high entry prices. Locking in your rate provides a "peace of mind" factor that shouldn't be underestimated. It's the smartest move if you plan to stay in your home long-term and don't want to monitor central bank announcements every six weeks.

The Strategy Behind Variable-Rate Mortgages

Smart variable strategies work best when you have a cash buffer. You need to understand your "trigger rate," the point where your monthly payment only covers interest and no longer reduces the principal. Because the Bank of Canada's policy rate is expected to hold at 2.25% through 2026, many borrowers feel confident that trigger rates won't be hit. Managing interest across all your debts is a cohesive skill. You can see how these principles apply to other sectors in our Auto Loans in Canada guide. This broader perspective helps you master total interest management across your entire financial life.

The Road to Approval: Pre-Qualification and Documentation

Securing a mortgage loan requires a high level of organizational discipline. Lenders need absolute certainty regarding your financial health before they commit capital. You can streamline this by following five essential steps: organizing your income proof, auditing your current debt, verifying your down payment source, calculating your debt-to-income ratios, and securing a formal pre-approval. Prepare your digital folder early. You'll need your most recent T4s, at least two years of Notices of Assessment (NOAs), and 90 days of bank statements to prove your down payment isn't a loan. Having these ready prevents the back-and-forth that often delays approvals.

AI-powered forms now handle the heavy lifting of the initial application. Instead of manual data entry that often leads to errors, these smart systems validate your information in real-time. This technology ensures that when a lender reviews your file, the numbers are accurate and the risk assessment is clear. It turns a weeks-long process into a matter of days, allowing you to move at the speed of the 2026 real estate market. This digital-first approach removes the friction from traditional lending, giving you a competitive edge when bidding on a property.

Step-by-Step Pre-Qualification Process

Start with pre-qualification. This is an initial estimate based on your self-reported data. It’s different from a pre-approval, which involves a deep dive into your credit history and verified income. You can pre-qualify through our platform without a hard credit pull, protecting your score while you explore your options. Lenders will look closely at your Gross Debt Service (GDS) and Total Debt Service (TDS) ratios. Keeping these below the standard thresholds of 39% and 44% respectively is the key to unlocking the best terms on your mortgage loan. If your ratios are high, consider paying down high-interest credit card debt before you apply.

Navigating Local Markets: From Kelowna to Edmonton

Local expertise is vital when moving between provinces. Buyers in Calgary and Edmonton enjoy a lower tax burden compared to those in Ottawa because Alberta does not charge a provincial land transfer tax. In contrast, Ontario buyers must budget for significant closing costs, sometimes reaching thousands of dollars. From Kelowna’s luxury market to the competitive entry-level homes in Richmond or Surrey, every city has unique bylaws and tax implications. Connecting with an agent who understands your specific municipality can save you from unforeseen costs. They know the local landscape and can guide you through municipal land transfer rebates that generalist lenders might miss. Ready to see where you stand? Check your pre-qualification status today and start your journey with confidence.

The QuoteShack Advantage: Why a Mortgage Marketplace Wins

Relying on a single bank limits your options to one set of internal criteria. A mortgage loan is a significant financial commitment, and settling for the first offer you receive can cost you thousands over the life of the term. Our marketplace model flips the script by forcing lenders to compete for your business. Instead of you chasing the best rate, the best rates find you. This competitive environment ensures you aren't just getting a standard product, but the most efficient financing structure available for your specific profile.

We empower lenders by providing them with high-fidelity data through our AI-powered smart forms. This technological bridge allows financial institutions to deliver faster, more accurate quotes because they aren't guessing about your eligibility. They receive a verified snapshot of your financial health, which results in more aggressive pricing and fewer processing delays. It turns the traditionally friction-filled application process into a seamless digital handoff.

Efficiency Through Technology

2026 borrowers prioritize digital-first financial tools that respect their time. AI-driven matching eliminates the need to visit multiple bank branches or repeat your story to different advisors. You gain absolute transparency by seeing multiple options within a single dashboard. This side-by-side comparison allows you to evaluate not just the interest rate, but the fine print that impacts your long-term flexibility. It’s about having a smart matchmaker that has already performed the complex background work for you.

Your Next Steps to Homeownership

Your mortgage loan is a tool for building generational wealth, not just a way to pay for a roof over your head. Taking the next step shouldn't feel like an obstacle. By using a single smart form, you reach a broad network of professionals ready to support your goals. Whether you're buying your first condo or upgrading to a family home, the right partner makes the difference between anxiety and empowerment. Start your mortgage pre-qualification with QuoteShack today and find the smartest path to your new front door.

Secure Your Financial Future in the 2026 Housing Market

The Canadian housing landscape is shifting. Success now depends on your ability to leverage data and technology. You've learned how to decode amortization schedules and navigate the 5.25% stress test with precision. Mastering the nuances of your mortgage loan isn't just about finding a house; it's about building a sustainable financial foundation. Choosing between fixed-rate certainty and variable-rate flexibility is a strategic decision that impacts your cash flow for years to come.

We remove the friction from this complex journey. Our platform uses AI-powered smart forms to ensure faster accuracy and connects you to a wide network of Canadian lenders. Trusted by borrowers in Toronto, Vancouver, and across the country, we specialize in making the path to homeownership transparent and fast. You don't have to navigate the renewal cliff or hidden fees alone when you have a capable partner by your side.

Stop guessing about your eligibility. Take control of your home-buying journey by using tools designed for the modern borrower. Check how much you pre-qualify for today and move forward with absolute certainty. Your smartest path to homeownership starts with a single, intelligent step.

Frequently Asked Questions

What is the minimum down payment for a mortgage loan in Canada?

You need a minimum down payment of 5% for the first C$500,000 of the purchase price and 10% for any portion between C$500,000 and C$999,999. If the home price is C$1 million or more, the law requires a full 20% down payment. This tiered system helps entry-level buyers enter the market with lower upfront capital while ensuring larger investments remain stable.

How does my credit score affect my mortgage interest rate?

Your credit score acts as a primary indicator of risk, where a higher score unlocks lower interest rates and more flexible terms. Most prime lenders look for a score of at least 680 to offer their most competitive products. If your score sits below this threshold, you may still qualify through alternative lenders, though you'll likely pay a higher rate to compensate for the perceived risk.

Can I get a mortgage loan if I am self-employed?

Yes, self-employed individuals can secure a mortgage loan by providing two years of Notices of Assessment (NOAs) to verify their income. Lenders prioritize consistency and look for a stable history of earnings within your industry. Using digital smart forms helps organize your business financial data, making it easier for lenders to assess your application through "proven income" programs.

What is mortgage loan insurance (CMHC) and do I need it?

Mortgage loan insurance is mandatory if your down payment is less than 20% of the home's purchase price. It protects the lender if you default on your payments, and the premium is usually added to your total loan balance. This insurance is the mechanism that allows Canadians to purchase property with as little as 5% down, though it does increase your total debt.

How much can I actually afford to borrow for a home?

Lenders determine your maximum loan amount using your Gross Debt Service (GDS) and Total Debt Service (TDS) ratios. These shouldn't exceed 39% and 44% of your pre-tax income respectively. Your affordability is also capped by the 5.25% stress test, which ensures you can still manage payments if interest rates rise. Use a pre-qualification tool to see your specific limit based on current debt.

What happens when my mortgage term ends?

You have the option to renew with your current lender, switch to a new lender for better rates, or pay off the balance entirely. With about 60% of mortgages renewing in 2025 and 2026, many homeowners face higher monthly payments than their previous term. Start your research six months before your maturity date to avoid being locked into a high "posted" rate by your existing bank.

Is it better to get a mortgage from a bank or a broker?

Banks only offer their own proprietary products, while a marketplace or broker provides access to a wide network of lenders through a single application. This marketplace model creates competition for your business, often resulting in lower rates and better terms. It's an efficient way to compare multiple options simultaneously without the friction of visiting several different bank branches.

How long does the mortgage approval process take in 2026?

Digital-first applications can secure a conditional approval in as little as 24 to 72 hours. Traditional manual processes often take up to 10 business days due to slower document verification. You can speed up this timeline by having your electronic T4s, bank statements, and employment letters ready. Our AI-powered forms ensure your data is accurate from the start, reducing the need for time-consuming follow-ups.