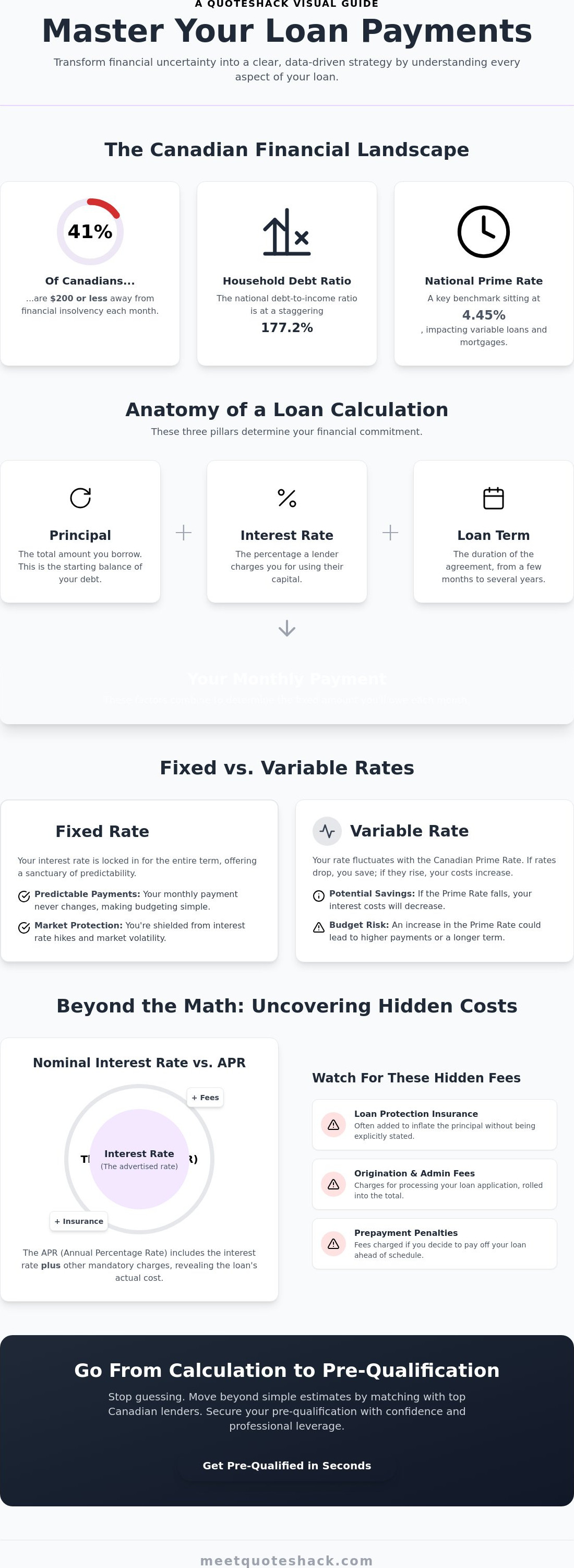

Did you know that 41% of Canadians are currently $200 or less away from financial insolvency every month? With the national household debt-to-income ratio sitting at 177.2%, managing your monthly budget has never been more critical. You're likely feeling the weight of a 4.45% prime rate and the stress of potential mortgage renewal shocks. Using a precise loan payment calculator transforms this uncertainty into a clear, data-driven strategy. It's the fastest way to see past the marketing jargon and understand exactly what you'll owe.

You deserve to know the truth about your financing before you sign any contracts. We'll show you how to decode the gap between APR and interest rates, spot hidden fees, and compare Canadian lenders side-by-side. This guide explores how to master these digital tools to secure the best terms for auto, personal, or home loans. You'll walk away with a predictable monthly budget and a direct path to pre-qualification. Let's turn complex financial math into your greatest competitive advantage.

Key Takeaways

- Use a loan payment calculator as a digital shield to identify predatory lending terms and visualize your long-term debt obligations.

- Distinguish between nominal interest rates and the actual APR to reveal the true cost of borrowing, including fees and insurance.

- Factor in Canadian-specific variables like vehicle depreciation and trade-in values to build a realistic monthly budget for auto or personal loans.

- Identify hidden costs like loan protection insurance and origination fees that basic calculation tools often overlook.

- Move beyond simple estimates by using QuoteShack to match with top Canadian lenders and secure pre-qualification in seconds.

What is a Loan Payment Calculator and Why is it Essential?

A loan payment calculator is more than a simple math application; it's a strategic digital tool designed to estimate your monthly instalments based on three core variables: principal, interest, and term. In a market where 41% of Canadians are on the verge of insolvency, this tool acts as your primary financial shield. It strips away the complexity of lending contracts to reveal the true cost of borrowing before you commit to a single dollar of debt. By visualizing the total interest paid over the life of the loan, you gain the transparency needed to avoid predatory lending structures that often hide in the fine print.

Using this technology allows you to experiment with different financial futures in seconds. You can see how a larger down payment reduces your long-term costs or how a slightly higher interest rate impacts your weekly budget. This clarity is vital for staying within the 14.57% debt service ratio that currently defines the average Canadian household. It's about taking control of the narrative before a lender does.

The Anatomy of a Loan Calculation

Every calculation relies on three pillars that determine your financial commitment. Understanding these helps you manipulate the variables to find a payment that fits your lifestyle. To understand how these factors interact through time, many experts refer to an Amortization calculator, which provides a detailed schedule of how each payment is split between principal and interest.

- Principal: This is the total amount you borrow for your car, home, or personal needs. It's the starting balance of your debt.

- Interest Rate: This is the percentage the lender charges for the privilege of using their capital. Even a 0.5% difference can cost you thousands over time.

- Loan Term: This is the duration of the agreement. While longer terms lower monthly payments, they significantly increase the total interest you'll pay.

Fixed vs. Variable Rates in the Canadian Market

With the Bank of Canada policy rate at 2.25% and the Prime Rate at 4.45% in May 2026, choosing the right rate structure is a critical decision. Fixed rates offer a sanctuary of predictability. They lock in your payment, protecting your budget from market volatility. Variable rates fluctuate alongside the Canadian Prime Rate. If rates drop, you save; if they rise, your monthly obligation or your total term could increase. In 2026, your choice should depend on your risk tolerance and whether your budget can absorb the "renewal shock" many Canadians are currently facing.

Comparison Power: From Brampton to Ottawa

Never step onto a car lot in Brampton or visit a mortgage broker in Ottawa without running your numbers first. Dealerships and lenders often focus on the monthly payment to distract you from high interest rates or extended terms. Armed with a loan payment calculator, you can challenge these offers in real time. You'll know exactly what a fair payment looks like based on your credit profile. Once you've established your baseline, you can check how much you pre-qualify for to approach lenders with total confidence and professional leverage.

How to Use a Loan Payment Calculator: A Step-by-Step Guide

Mastering a loan payment calculator requires more than just plugging in random numbers. It demands a tactical approach to data entry to ensure the results reflect your actual financial reality. Start by gathering your current credit score. In May 2026, personal loan interest rates typically range from 6% to 35% APR. Knowing where you land on this spectrum prevents you from overestimating your borrowing power or, conversely, accepting a sub-optimal deal. Once you have your baseline, follow these steps to build your financial roadmap.

- Define the Principal: Input the total amount you need to borrow. Be realistic by subtracting your down payment or trade-in value from the purchase price.

- Select Your Term: Choose a duration that balances monthly affordability with long-term savings. While an 84-month term lowers your immediate bill, it drastically increases the total interest paid.

- Adjust Payment Frequency: Compare monthly payments against accelerated bi-weekly or weekly schedules. Increasing frequency can shave months off your debt and save hundreds in interest.

- Review the Amortization: Examine the first-year breakdown. Seeing how little principal you clear in the early stages of a high-interest loan is often the reality check needed to reconsider your budget.

Inputting Your Data for Maximum Accuracy

Your credit score is the most influential variable in this equation. For instance, while the average car loan interest rate is 6.72% as of May 9, 2026, your specific rate could be much higher or lower based on your history. To practice these steps and see how variables shift, you can explore the Office of Financial Readiness Loan Calculator to visualize different scenarios. Use the calculator to determine your "ceiling"-the maximum purchase price that keeps your debt service ratio below 15% of your disposable income. This proactive step ensures you only shop for what you can truly afford.

Interpreting the Results: Monthly vs. Total Cost

Avoid the "Monthly Payment Trap." Lenders in competitive markets like Toronto or Vancouver often focus on a low monthly figure to make expensive loans seem attractive. Always look at the "Total Interest Paid" field. This is the true price of the loan. If a C$30,000 auto loan costs you C$12,000 in interest over seven years, the "deal" loses its luster. Use these calculated figures as leverage during negotiations. When you show a lender you've already decoded their math, you're positioned as an informed, low-risk borrower. To take the next step, check how much you pre-qualify for to see real-world rates tailored to your profile.

Securing the right financing is about speed and intelligence. If you are ready to compare actual offers from across the country, you can start your search today to find a match that fits your strategy.

Strategic Scenarios: Auto, Personal, and Mortgage Loans

Numbers remain abstract data points until you apply them to your specific financial goals. A loan payment calculator functions as a strategy engine, allowing you to simulate real-world outcomes before committing to a contract. Whether you're upgrading a vehicle in Calgary or managing a mortgage renewal in Victoria, these tools provide the foresight needed to avoid expensive mistakes. By testing different scenarios, you can identify the exact moment a loan becomes a burden rather than a benefit.

For those considering smaller, unsecured borrowing, the Forbes Personal Loan Calculator offers a reliable way to estimate costs for emergency repairs or home improvements. This proactive planning is essential in 2026, as Canadians continue to grapple with a high household debt service ratio of 14.57%. Moving beyond simple math helps you align your borrowing with your actual cash flow.

Optimizing Your Auto Loan Strategy

Vehicle financing in Canada requires a balance between monthly cash flow and long-term asset value. If you're eyeing a new SUV in Calgary, you might be tempted by an 84-month term to keep payments low. However, a loan payment calculator reveals the hidden cost: you could end up paying thousands more in interest while the vehicle's value depreciates faster than you can pay down the principal. Compare a 60-month term against an 84-month term to find the "sweet spot" where you maintain equity. Always factor in your trade-in value to reduce the principal from the start. For a deeper dive into these nuances, read our Auto Loans Guide.

Consolidation Strategy: Seeing the Savings

With nearly half of Canadians reporting an increase in debt over the past year, consolidation has become a vital survival tool. Use a calculator to aggregate your high-interest credit card balances into a single personal loan. The visual impact is often immediate. You'll likely see a single monthly payment that is significantly lower than the sum of your current minimums. This strategy doesn't just simplify your life; it accelerates your path to a zero balance by focusing your capital on a lower-interest environment. You can learn more about loans and debt consolidation to see if this path fits your 2026 recovery plan.

Mortgage Refinancing and the Break-Even Point

Approximately 33% of Canadian mortgage holders are expected to face a "renewal shock" in 2026, with monthly payments potentially jumping by 20%. Use your calculation tools to find the break-even point when considering a refinance. This is the moment where the interest savings from a lower rate finally outweigh the penalties and closing costs of breaking your current term. If you don't plan to stay in the home past that date, refinancing might not be the right move. If you're ready to see how these numbers apply to your situation, you can check how much you pre-qualify for to get a head start on your next application.

Beyond the Math: Hidden Costs Most Calculators Ignore

A basic loan payment calculator provides a vital baseline, but it rarely accounts for the granular expenses that appear on your final contract. To build a truly bulletproof budget, you must look past the interest rate and identify the secondary costs that lenders often fold into the fine print. These additions can shift your monthly obligation by hundreds of dollars, turning an affordable plan into a financial strain. Recognizing these factors early allows you to negotiate with total clarity.

The most significant discrepancy is the gap between the nominal interest rate and the Annual Percentage Rate (APR). While the interest rate covers the cost of borrowing the principal, the APR includes mandatory fees such as origination charges or administrative costs common in Canadian personal loans. Always use the APR for your final calculation. It represents the "all-in" cost of your debt, ensuring you don't face a surprise on your first statement. Other invisible hurdles include:

- Loan Protection Insurance: This optional coverage protects your payments during job loss or illness but adds a recurring premium to your balance.

- Pre-payment Penalties: Some lenders charge fees if you pay off your loan early. This is particularly common in the mortgage market and can cost thousands.

- Origination Fees: These are one-time processing charges, often ranging from 1% to 5% of the loan amount, deducted before you even receive the funds.

The Bank of Canada and Your Interest Rate

The Bank of Canada policy rate, currently holding at 2.25% as of May 2026, dictates the floor of your borrowing costs. This rate directly influences the 4.45% Prime Rate used by major banks. For residents in markets like Kamloops or Kelowna, staying ahead of these trends is essential for timing a loan application. Because these rates fluctuate, a loan payment calculator result is only an estimate until you secure a formal offer. Pre-qualification is the only way to lock in a firm rate tailored to your specific credit profile and regional market conditions.

Factoring in Regional Taxes and Fees

Provincial regulations also shift the math. When calculating an auto loan, remember that sales taxes like GST or HST vary significantly across the country. A vehicle purchase in Surrey involves different tax obligations and dealership documentation fees than one in Calgary. Similarly, mortgage refinancing in high-volume cities often comes with higher appraisal and legal closing costs. Always include a 5% to 10% "buffer room" in your calculated budget to absorb these localized expenses without breaking your plan.

The best way to see your actual costs is to move from estimates to real-world offers. You can find the best Canadian lenders and get a transparent view of your financing options in seconds.

The QuoteShack Advantage: From Calculation to Funding

A loan payment calculator provides the essential blueprint for your financial future, but it cannot execute the build. You have already decoded the interest rates and visualized the impact of different terms on your monthly budget. Now, you need a partner to turn those theoretical estimates into a funded reality. QuoteShack bridges this gap by connecting your calculated goals with actual Canadian lenders in seconds. We remove the friction of manual searching, allowing you to move from curiosity to capital with professional speed and precision.

Borrowers in Toronto or Ottawa shouldn't have to spend hours filling out repetitive applications at different banks. Our platform utilizes high-tech AI smart forms to capture your data once and match it against a network of vetted institutional partners. This isn't just about finding a loan; it's about finding the right match for your specific credit profile and 2026 market conditions. By leveraging our intelligent facilitator, you gain access to competitive rates that a generic search might miss. We do the heavy lifting so you can maintain your momentum.

One of the most powerful tools in your 2026 financial strategy is pre-qualification. It allows you to see real numbers and firm offers without the risk of a hard credit pull. You get the reassurance of knowing exactly where you stand before you start shopping for a home or vehicle. It is the final step in validating the data you gathered from your loan payment calculator. Transitioning from "what if" to "here is the offer" has never been more seamless.

Move Past Estimates with Smart Matching

Our system effectively bridges the gap between Vancouver borrowers and national lenders. Whether you are looking for a debt consolidation loan or a mortgage refinance, our intelligent matchmaking service ensures you aren't limited by your local branch's criteria. You can explore our loanee solutions to see how we personalize the lending experience for every Canadian province. We handle the complex background work and present you with a simplified path forward.

Secure Your 2026 Loan Today

Before you finalize your application, perform a final comparison. Align your initial calculator results with the firm lender offers you receive through our platform. Check the APR, total interest, and any regional fees to ensure the deal matches your strategy. When the numbers align, you can apply with total confidence. Ready to see what you qualify for? Get your custom quotes now and secure the financing you need to grow.

Take Control of Your 2026 Financing Strategy

Financial clarity is your most valuable asset in a volatile market. You now have the expertise to use a loan payment calculator to peel back the layers of complex lending contracts. By identifying the real APR and accounting for regional fees, you've transformed from a passive borrower into a strategic decision-maker. You understand how to balance monthly affordability with long-term interest savings; this ensures your debt remains a tool for growth rather than a burden.

The transition from calculation to funding should be just as precise. QuoteShack simplifies this final step through AI-powered smart matching and direct access to a national network of professional mortgage advisors. Our no-obligation pre-qualification tools provide the real-world numbers you need without affecting your credit score. It's the fastest way to validate your strategy and secure the best possible terms across Canada. You've already performed the difficult background work. Now, it's time to let technology bridge the gap to your goals.

Calculate your real loan options and pre-qualify today at QuoteShack. You've run the numbers and built your plan. Take the next step with confidence and secure the financing you deserve.

Frequently Asked Questions

Is the monthly payment from a calculator guaranteed by lenders?

No, calculator results are estimates and not guaranteed offers. Lenders determine your final payment based on your specific credit history, income verification, and internal risk assessments. While a loan payment calculator provides a reliable baseline, you only get a firm commitment after a formal application or pre-qualification process. Always treat these digital estimates as a starting point for your budget rather than a final contract.

How does a longer loan term affect the total interest I pay?

Extending your loan term reduces your monthly obligation but increases the total interest paid over time. For example, moving from a 60-month to an 84-month auto loan might make the payment feel manageable, but it often adds thousands of dollars to the cost of the vehicle. You are essentially paying for the convenience of a lower monthly bill with a much higher total price tag at the end of the term.

What is the difference between a loan interest rate and the APR?

The interest rate is the basic cost of borrowing the principal amount. The Annual Percentage Rate (APR) is a broader figure that includes the interest rate plus mandatory fees, such as origination charges or administrative costs. Because the APR reflects the "all-in" cost of the loan, it is the most accurate number to use when comparing different Canadian lenders side by side.

Can I use a loan payment calculator for a mortgage refinance in Canada?

Yes, calculators are essential for determining the viability of a mortgage refinance. You can input your new potential rate, such as the 3.84% fixed rate available in May 2026, and compare it against your current payment. This helps you identify the "break-even" point where your interest savings finally exceed the legal fees and penalties associated with breaking your original mortgage contract.

Do I need to include my trade-in value in a car payment calculator?

Yes, you should subtract your trade-in value and any down payment from the vehicle's purchase price before calculating. This reduced figure is the actual principal you need to finance. Lowering the principal directly reduces both your monthly payments and the total interest accrued over the life of the loan. It is one of the most effective ways to make a new vehicle purchase more affordable.

How often do Canadian interest rates change in 2026?

The Bank of Canada typically reviews interest rates eight times per year. In May 2026, the policy rate sits at 2.25%, with the Prime Rate at 4.45%. While these rates are currently stable, fluctuations can occur after any scheduled announcement. Keeping a close eye on these dates is vital for anyone planning to use a loan payment calculator to time their next major loan application or renewal.

Does using an online loan calculator affect my credit score?

No, using an online calculator is a private activity that has zero impact on your credit score. These tools don't communicate with credit bureaus like Equifax or TransUnion. You can run as many scenarios as you like to find your ideal budget. Only a formal application involving a hard credit pull by a lender will affect your credit rating.

What is a good interest rate for a personal loan in Ontario right now?

A good rate in Ontario depends heavily on your credit score, but competitive personal loan rates in May 2026 often start around 6% to 10% APR for high-credit borrowers. With the average personal loan range spanning up to 35%, securing a rate in the single digits or low teens is considered favorable. Your final rate will reflect your debt-to-income ratio and the lender's current risk appetite.